Amit Anand (NextFins)

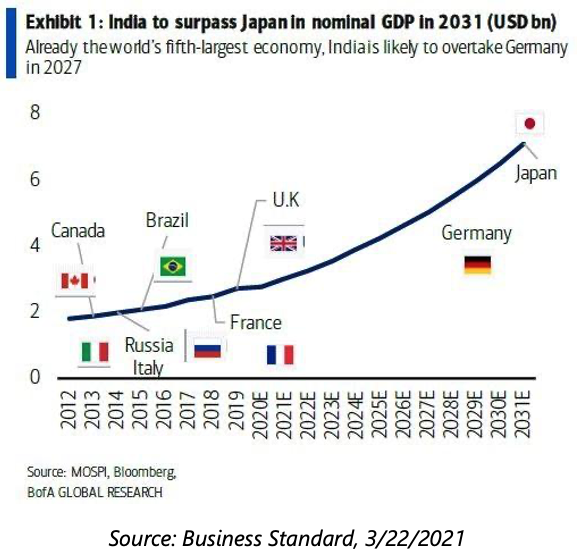

India, the world’s fifth largest economy[1], is expected to become the third largest economy by the end of the decade[2]. India’s GDP is expected to grow 7.7% in 2022 and another 6.0% in 2023, making India the fastest growing major economy in the world.

Importantly, India’s growth is underpinned by structural megatrends as opposed to short-term stimulus funded by money printing. Specifically, India’s young population (median age of 28) is contributing to a growing workforce that is interested in consuming, traveling and investing. Low data rates and cheap smartphones are allowing Indians to leapfrog straight into the world of e-commerce, fintech and social media. India’s new 17% tax rate for manufacturing companies make the country a preferred destination for factories seeking a China alternative.

India has a deep equity market, with over 4,600 publicly listed companies and over 1,000 public companies with a market cap of over $100mm[3]. In a market with so many available opportunities, how does an investor decide what stocks are worth owning? Generally, every country has a theme that consistently outperforms and the reasons for outperformance are structural in nature.

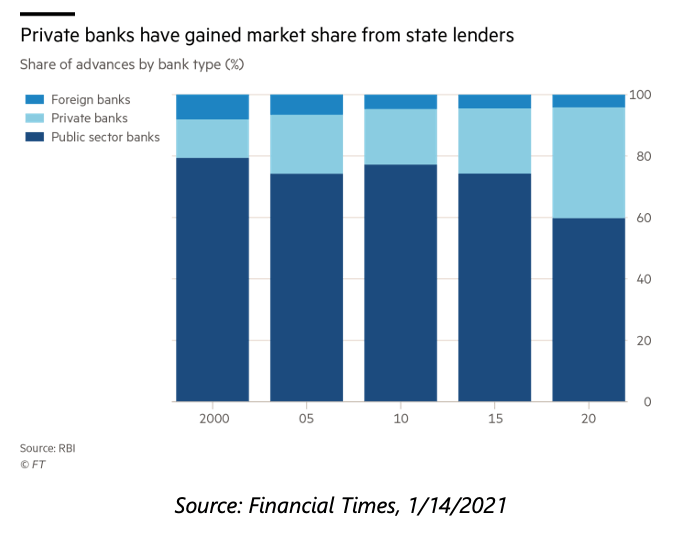

In India, we believe the theme worth owning is financial companies. Financial companies include primarily the large private sector banks but also fintech, housing finance, consumer credit and insurance companies. India’s bank credit has historically grown at a multiple of GDP, so the rising tide of economic growth helps all boats, but particularly the financials. Furthermore, India has a two-class banking sector: private sector banks and state-run banks. There are 21 private sector banks in operation today, and new banking licenses are extremely hard to come by (the regulator is wary of industrialists starting banks for their own benefit).

Private sector banks started with 0 market share when they were first allowed to exist in the early 1990s; since then, they have consistently gained share and now account for about 37% of the total credit outstanding in the Indian banking system[4]. So not only do the financials grow at a multiple of GDP growth, the private sector banks that can take share from state-run banks grow at a multiple of the financial sector as a whole.

The unique characteristics of Indian private sector financials haven’t gone unnoticed by the market. The Nifty Financial Services 25/50 Index has compounded at 17.47% annually over the last five years[5] (as of November 30, 2021). Importantly, looking forward, consensus estimates call for the financial sector to deliver 26% earnings per share (EPS) growth in 2022, which is ahead of the consensus estimates of 15% EPS growth for MSCI India as a whole[6].

[1] https://www.businesstoday.in/latest/economy-politics/story/india-surpasses-france-uk-to-become-world-5th-largest-economy-imf-250640-2020-02-23

[2] https://timesofindia.indiatimes.com/business/india-business/india-to-become-3rd-largest-economy-by-2030-report/articleshow/79972584.cms

[3] Source: S&P CapitalIQ, as of 11/20/2021.

[4] https://www.business-standard.com/article/finance/private-sector-banks-share-in-loans-rises-to-36-5-in-fy21-121062901617_1.html

[5] https://www.niftyindices.com/Factsheet/Factsheet_Nifty_FinServ_25_50.pdf

[6] Source: Goldman Sachs, “India Weekly Kickstart”, 11/19/2021