Amit Anand (NextFins)

Follow Amit on LinkedIn @amit-anand

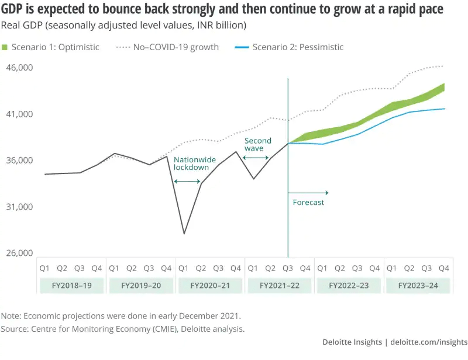

After a series of setbacks, primarily relating to successive waves of the Covid pandemic, India is poised to resume its upwards trajectory of GDP growth.

However, over the last twelve months, investors have been reminded once again that economic growth doesn’t simply result in stock market appreciation. The importance of understanding government policy is key when it comes to making money in emerging market stocks.

Amidst the BRIC countries (Brazil, Russia, India, China), which in recent times have represented the majority of investors’ emerging markets exposure[1], India stands apart in offering investors increased visibility on where policy is headed. This increased visibility is the result of recently concluded local elections, which – although received modest coverage in US media – carried immense importance for India.

The state of Uttar Pradesh, which has a population of over 200 million people, went to the polls in February and March to elect its legislative assembly in what is likely the largest local election in the world. Uttar Pradesh has a history of being famously anti-incumbent, with no political party being able to retain its majority since 1985. The incumbent party in this election was the same party that has the national majority – the BJP. Angst around the government’s handling of the Covid pandemic, an unsuccessful attempt at reforming farm laws, as well as the state’s history of anti-incumbency had pollsters predicting significant losses for the ruling party. Nevertheless, the BJP ended up securing a comfortable majority in the local assembly which gives it increased momentum heading into the national elections in 2024.

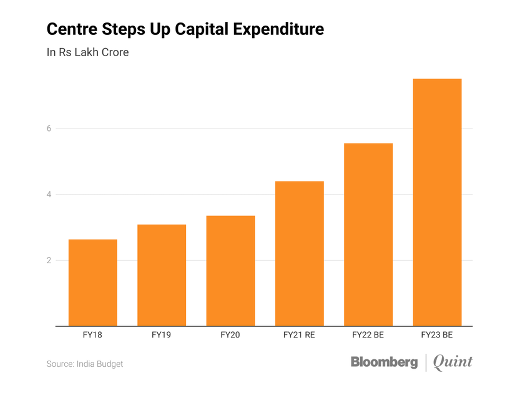

Looking forward, the BJP-led government is likely to continue its policy to foster economic growth. After a significant corporate tax rate cut in 2019, the government is now focused on boosting capital expenditures to create jobs and catalyze India’s corporations to step up their own capex. In its budget for FY 2023, which runs through March 2023, the government proposed increasing capex by 35% compared to FY 2022.

To pay for higher capex, the government has launched a program of privatizing state-owned assets. In 2021, the government sold the national carrier Air India to the Tata Group. In 2022, it is planning to IPO Life Insurance Corporation of India (LIC), which has the #1 market share in India’s nascent but growing life insurance sector. Analysts have estimated that LIC could be worth $200bn, which would instantly make it the second largest publicly listed company in India.

The government’s policy of recycling capital from underperforming or inefficient state-controlled assets to new infrastructure such as green energy, roads and special economic zones is effective portfolio management, not just for the government’s finances, but also for India’s future.

What does this mean for Indian Financials?

Indian financials are the largest sector by weight in the Indian benchmark index and have historically been the crown jewels of the Indian stock market. Indian financials are GDP-sensitive companies and hence policies that support GDP growth tend to benefit the financial sector (historically, overall bank credit in India has grown at a multiple of GDP growth).

Credit growth in recent years has been driven by consumer borrowing (mortgages, auto loans and credit cards), while corporate credit growth has been tepid. If increased government spending on capex also leads to a corporate capex cycle, Indian financials can potentially experience faster growth going forward.

The largest Indian banks by market cap are also asset-sensitive, which means their earnings benefit when interest rates rise. To the extent inflation expectations in India rise as a result of faster growth, investors may start pricing in interest rate increases and earnings upgrades for Indian financials.

[1] As of February 2022, these countries represented approximately 50% of the EM benchmark index.